-landscape")

See full Titanium Market Overview (USGS) Infographic here.

The global titanium market has reached a turning point in its development: on the one hand, Russia, one of the main producers of titanium, is facing sanctions imposed by the European Union, the United States and their satellites; on the other hand, global demand for the metal is growing and will be difficult to meet without Russian supplies.

Growth amid problems

VSMPO-AVISMA Corporation is planning to build a bar rolling complex in the Titanium Valley special economic zone (Sverdlovsk Region). Construction is due to begin by the end of this year, with operations scheduled to start in 2027. The cost of the VSMPO-AVISMA project is estimated at $214.5 million and will be the largest in the Russian titanium industry in the past decade.

VSMPO-Avisma, Russia’s largest titanium producer and one of the world leaders, didn’t come up with the idea by chance. The residents of Titanium Valley enjoy a range of tax and customs benefits and concessions that enable them to accelerate the return on their projects.

The future bar rolling complex will ensure serial production of high quality titanium products of small diameters for advanced projects in aviation, shipbuilding and medicine, thus helping to eliminate the need to import foreign products for the domestic industry. The project will allow VSMPO-AVISMA to double its own titanium bar production capacity, expand its product range and meet the growing demand of the Russian market.

In early July, VSMPO-AVISMA opened a workshop for machining titanium alloy rings and discs. The $32.7 million investment project was implemented over three years. In the first stage, a line for semi-finished machining of rings and discs for aircraft and engine construction was built, while in the second stage, equipment for final machining will be put into operation.

VSMPO-Avisma has to carry out such projects in the midst of Western sanctions. In March last year its long-time partner, the American aircraft manufacturer Boeing, officially announced the suspension of existing contracts for the purchase of titanium from VSMPO-Avisma. At the same time, Boeing announced the urgent creation of a pool of titanium suppliers who could meet the criteria of Russian products. There was nothing else Boeing could do, because at that time it was 30% dependent on titanium from VSMPO-AVISMA, which it used in the production of key aircraft models — Boeing 767, Boeing 737 Max and others.

In December 2022, European aviation giant Airbus, which met 60% of its own needs for titanium from VSMPO-AVISMA, announced its plans to stop buying titanium from the company. As an alternative, it is considering producers in Japan and the US. On the other hand, the Brazilian manufacturer Embraer did not follow the example of Boeing and Airbus — it is 100% dependent on VSMPO-Avisma titanium.

In total, VSMPO-AVISMA produced 34.5 thousand tonnes of titanium in 2022, and this year its output may increase to 37 thousand tonnes due to strong demand in the Russian domestic market.

Real import substitution

Apart from VSMPO-Avisma, there is another titanium producer in Russia — Solikamsk Magnesium Plant (SMZ). Its production of the metal is rather modest — 1.5 thousand tonnes in 2022, with a capacity of 5 thousand tonnes. Moreover, SMZ only produces titanium sponge, while VSMPO-AVISMA produces sponge, ingots and semi-finished products based on it. SMZ’s main products are magnesium and rare earths.

Despite its small titanium production, SMZ made a big splash in Russia in 2022: following a lawsuit filed by the Russian Prosecutor General’s Office, the company’s privatisation in 1992 was declared illegal by the court and its shares were transferred to state ownership. In 2023, SMZ was transferred to the state corporation Rosatom.

In terms of titanium ingot production capacity, VSMPO-AVISMA is undoubtedly the leader — it can produce up to 72,000 tonnes of titanium ingots per year. Another 5,000 tonnes can be produced by the Chepetsky Mechanical Plant (ChMZ, part of Rosatom), 2,000 tonnes by Ruspolymet and the same amount by the Stupino Metallurgical Company.

Russia imports titanium products from China only in small quantities: 900 tonnes in 2022, mainly powder, bars, wires, plates and tubes.

However, in the next few years we can expect these imports to cease due to the growth in the production of titanium semi-finished products at Russian enterprises — in addition to the aforementioned VSMPO-AVISMA project to create a bar rolling complex in Titanium Valley, the Chelyabinsk Metallurgical Plant is expanding its existing capacity to produce titanium bars for the needs of various civilian industries — medicine, etc. — in order to meet the growing demand for titanium products.

Silence of the market makers

Against the backdrop of changes in the global titanium market over the past year and a half, Western companies are trying to strengthen their positions, taking advantage of the situation regarding sanctions against Russia. In July this year, for example, the American company Allegheny Technologies announced plans to increase production of titanium products at its plant in Richland (Washington State). The implementation of its investment project will increase production of semi-finished products for the aerospace and defense industries by 35% compared to 2022. The project is expected to be completed in 2024, with certification expected in 2025.

According to Allegheny Technologies, the Richland expansion will increase the supply of titanium products to companies that manufacture aircraft engines and parts. Interestingly, the project includes providing Richland with carbon-neutral electricity from hydroelectric plants.

Allegheny Technologies does not specify who exactly will receive the semi-finished titanium products once the project is completed, although it is easy to guess — probably Boeing, Lockheed Martin and other players working to meet the needs of US national defense.

This is evidenced by Allegheny Technologies’ contract with Bechtel Plant Machinery to produce components for the US Navy’s nuclear propulsion development programme. To meet its obligations, Allegheny Technologies will build a dedicated titanium fabrication facility in the state of Florida.

The facility will manufacture components using 3D printing, perform thermal and mechanical processing, and establish titanium powder production. It is expected to be operational by the middle of next year.

In contrast to Allegheny Technologies, two other major US titanium manufacturers, Timet and Howmet Aerospace, are reluctant to disclose their own projects and business, but it seems they are also trying to increase their influence on the global market.

Smaller players, on the other hand, are more open. Among them is IperionX, which in September 2023 signed an agreement with the Canadian company Heroux-Devtek to supply it with titanium obtained by remelting scrap.

Heroux-Devtek specialises in the design, development, manufacture and repair of landing gear for civil and military aircraft. It will collect the Ti-6Al-4V alloy scrap generated during the production of landing gear parts and supply it to IperionX. IperionX will recycle it and sell back to Heroux-Devtek.

Limitations

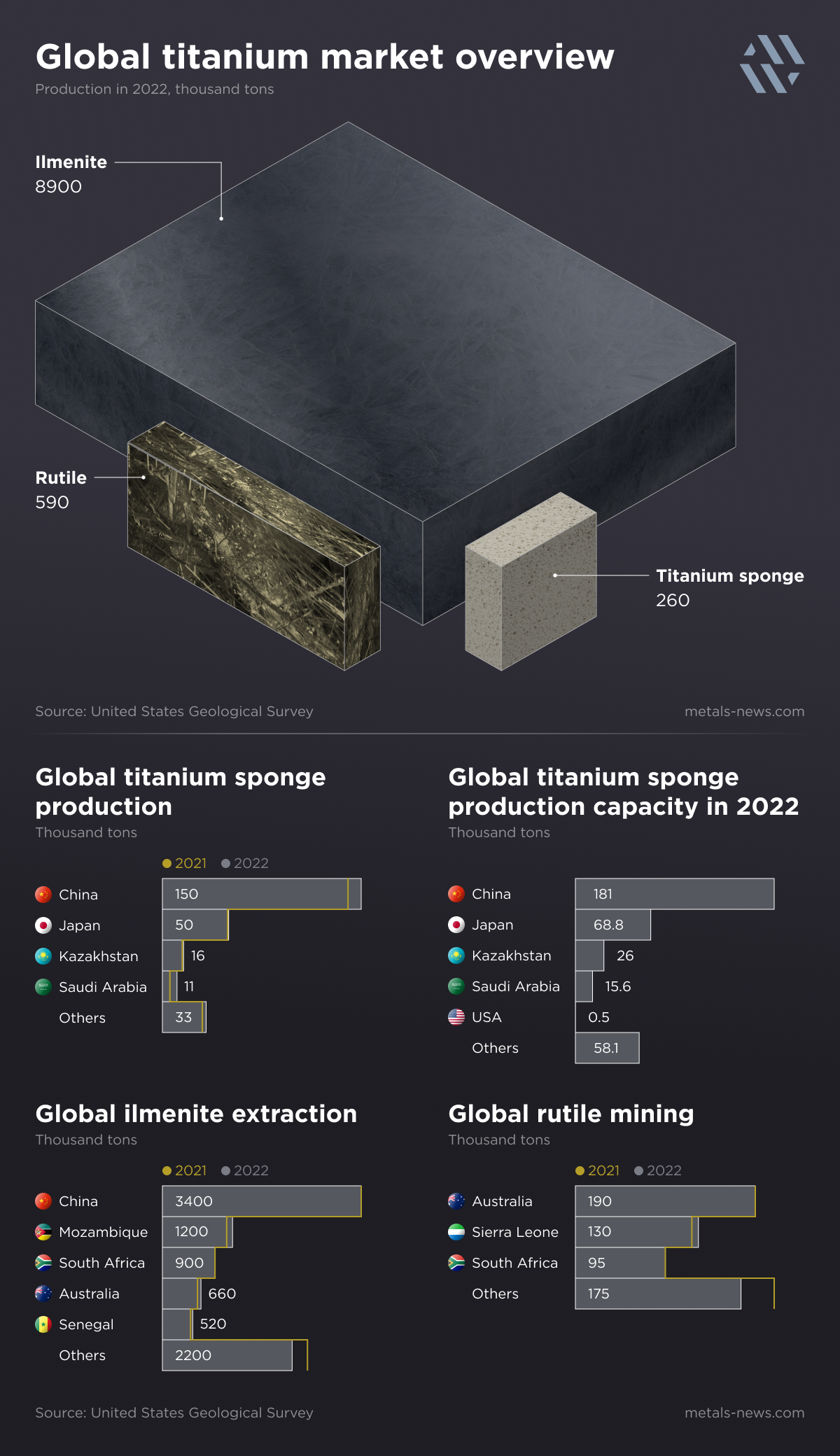

It’s worth noting that titanium ore production has not increased in recent years and is actually split between two minerals — ilmenite and rutile. According to the US Geological Survey, 8.9 million tonnes of ilmenite and 600,000 tonnes of rutile are mined annually worldwide. China, Mozambique, South Africa, Australia and Senegal dominate the ilmenite production structure, while Australia, Sierra Leone and South Africa dominate the rutile production structure.

The picture is quite different for titanium sponge (the basis for the production of ingots, semi-finished and finished products). According to the U.S. Geological Survey, the world production of titanium sponge in 2022 will amount to 260 thousand tonnes, which is only 8.3% more than in 2021. The largest volume of its production was observed in Japan, Kazakhstan, Russia, China and Saudi Arabia, and its increase was recorded in the last two countries.

At the same time, the production of titanium sponge in the United States itself is unknown, but it is unlikely to have increased significantly. The world’s existing sponge production capacity remained unchanged — estimated by the US Geological Survey at 350,000 tonnes.

If we compare them with the production volumes of titanium sponge, the underutilisation in China in 2022 will be 17%, in Japan — 26.5%, in Kazakhstan — 36.5%. Data on the situation in the United States are again not provided, although the U.S. Geological Survey puts the value of capacity at 500 tonnes per year and shows a jump in imports of titanium sponge by 75% to 28 thousand tonnes in 2022.

Several logical conclusions can be drawn. Boeing’s refusal to cooperate with Russia’s VSMPO-AVISMA was not accompanied by an increase in the production of titanium sponge in the United States, and American metallurgical companies had to buy it from Kazakhstan, China, Saudi Arabia and Japan to meet the demand of Boeing and other American consumers.

Suppliers from Kazakhstan and Japan simply could not fully replace Russian semi-finished titanium products on the world market due to a lack of available capacity. Their Chinese competitors were unlikely to supply large quantities of such products to the US market because of foreign policy and trade tensions between the two countries.

The members of the European Union and the UK do not have the capacity to produce large quantities of titanium sponge, ingots and semi-finished products and will certainly not be able to dramatically increase this capacity in the coming years — this would require huge investment and the construction of new metallurgical plants in a short period of time. Neither the European Union nor the UK will be able to supply enough.

The reshuffling of the major players on the world market is not accompanied by the expansion of titanium ore production and the launch of projects to develop promising deposits. There are very few sites with easy mining and geological conditions for development and large reserves of titanium, and most likely they have already been secured. Metallurgical producers will have to find a way out — either by paying higher prices for raw materials and competing with titanium white producers, or by trying to incorporate more scrap in processing, despite the limited availability of resources.

It is possible to predict an increase in the production of titanium powder products using 3D printing as a substitute for parts produced by traditional machining methods — cutting, welding, etc. However, it will be some time before they become a fully-fledged alternative to traditional methods. ![]()

{kind=link}